ELSS vs PPF: The Night I Rushed a Tax Decision and Regretted It Later

I didn’t plan to learn about money that night. It was around 10:45 PM, and I was sitting on my bed with my laptop, half-tired after a long day. My phone kept buzzing with WhatsApp messages from the office group which said – Guys, last date for tax proof submission this week

I opened my salary structure file and stared at the numbers like they would magically rearrange themselves. They didn’t. The reality was simple — if I didn’t invest under Section 80C immediately, a noticeable chunk of my salary was going to vanish into taxes.

I didn’t want that I wasn’t thinking about long-term wealth, retirement, or disciplined investing. I was thinking like most people do in that moment: How do I save tax right now?

A Half-Aware Decision

I started Googling and asking around. Two options kept coming up again and again — ELSS and PPF.

PPF sounded familiar. My parents had always trusted it. It was safe, long-term, and predictable. But to me, it felt… slow. ELSS, on the other hand, sounded modern. Fast. Smarter. People around me used words like “market growth” and “better returns.”

That’s all it took. At 11:30 PM that same night, without really sitting with the decision, I invested my entire tax-saving amount into ELSS.

Click- Confirm-Done and I remember closing the laptop with a strange sense of satisfaction, like I had just outsmarted the system.

The Silence Before Doubt

For a few weeks, nothing happened and that was the problem. Because in my mind, something should happen. I had just made an “investment,” after all.

So slowly, curiosity started creeping in.One evening, I opened the app and checked my portfolio. The number didn’t excite me. It also didn’t scare me. It was just… there.

But something inside me shifted.I started checking it more often than I needed to.

The First Realization

The first real moment of discomfort came when I checked it one morning before work and saw that the value had dropped slightly. It wasn’t a dramatic fall. If it had been any other expense in my life, I wouldn’t have even noticed. But this felt different. Because this wasn’t money I had spent. This was money I had “invested.” So It need to get return.

Can you understand what I just did here?

When “Returns” Start Feeling Personal

Over the next few months, I developed a habit I didn’t like — checking my investment too often. I wasn’t just observing anymore. I was reacting.

On days when the value went up, I felt validated. On days when it dipped, I felt uneasy, even if it was a small change.

That’s when I understood something no article had told me clearly before — market-linked investments are not just about returns, they are about temperament and I hadn’t checked mine.

A Small Conversation That Stayed With Me

One weekend, I was visiting home.My father was filling out some forms at the dining table. I noticed the familiar term — PPF — written neatly.

I casually said, “PPF is not giving much return dad, why are you still investing in it”

He didn’t answer immediately. He just finished writing, closed the file, and said something very simple:

“I don’t invest to impress anyone. I invest to sleep peacefully.” That line didn’t sound like financial advice but it affected me more than any comparison chart ever could.

Seeing Both Options Clearly for the First Time

That day, I stopped thinking in terms of “better” and “worse.” Instead, I started seeing ELSS and PPF for what they actually are. ELSS is not a shortcut. It’s a long-term commitment to equity markets. It needs time, patience, and the ability to ignore short-term noise.

PPF is not outdated. It’s structured stability. It’s predictable, consistent, and doesn’t demand your attention every week. One grows faster but moves unpredictably. The other fund grows slower but never makes feel fear or anxious.

The real difference is not in returns. The real difference is in how they make you feel over time.

How to select a best mutual fund — CLICK HERE

Where I Truly Went Wrong

I didn’t lose money that year in any major way but I lost something more important — clarity.

I had made a decision without understanding my own comfort level. I assumed I could handle volatility just because I liked the idea of higher returns.

But liking the idea and living the reality are two very different things.

The Change That Made a Difference

The following financial year, I did something I had never done before. I started early.

Not in February. Not in panic mode. I started in April and this time, I didn’t go all in on one option.

I split my approach.A part of my money went into ELSS, but through small monthly investments instead of one lump sum. The rest went into PPF. There was no excitement when I did this. No feeling of being “smart.”

But there was something new — calmness..

Income Tax website of India — > CLICK HERE

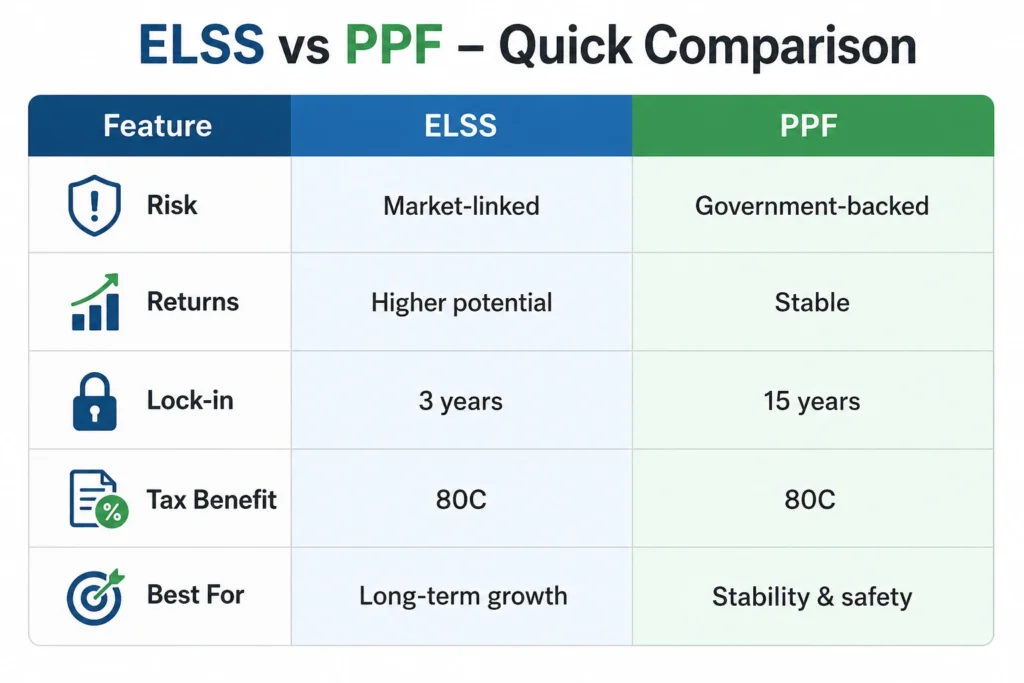

ELSS vs PPF – A quick comparison :-

You can check the quick comparison for ELSS vs PPF by seeing the below table in Image

A Quiet Shift in How I Felt About Money

Months passed, Markets moved. News changed. Life stayed busy. But one thing was different — I stopped obsessing over my investments. Because now, I wasn’t depending on just one outcome.

If markets dropped, everything wasn’t affected. If markets rose, I still benefited. That balance didn’t just change my portfolio. It changed my behaviour and in the long run, behaviour matters more than returns.

If You’re Reading This While Rushing

If you’re in that same situation I was in — late night, laptop open, trying to figure out how to save tax before the deadline — I completely understand. I wish someone had told me that night: that night this: –

Don’t treat tax saving like a last-minute task. Because when you rush, you don’t choose what suits you — you choose what sounds convincing in that moment.

And that decision stays with you longer than the tax season itself.

What Stayed With Me After That Year

I still invest in ELSS. I still invest in PPF.

But the difference is, now I know why each one is part of my life. One helps me grow.

The other helps me stay grounded. The experience which I received from this.

The best investment is not the one that looks impressive for a year. It’s the one you can stick with, without second-guessing yourself every month. That night, I thought I was making a smart move.

In reality, I was just making a fast one. It took time — and a little discomfort — to understand the difference.

Author

I am Livin Rangasamy, an Author, Engineer, AMFI ( Association of mutual funds in India) registered Mutual fund distributor and a guy who is more interested to teach finance to people who are interested.

Disclaimer

This content is meant for general understanding only and should not be taken as financial advice. It’s always better to do your own research or consult a professional before investing

For More similar posts :- CLICK HERE

")

")