Mutual Funds vs Fixed Deposits: What I Realized After Trying Both

For the longest time, whenever I had extra money sitting in my bank account, I would immediately move it into a fixed deposit.

That’s what most people around me trusted.

Parents trusted FDs. Relatives trusted FDs. Banks constantly promoted FDs as the safest way to grow savings.

So naturally, I believed:

“Keeping money safe is the smartest financial decision.”

And honestly, there’s nothing wrong with that thinking. Fixed deposits helped me build the habit of saving money consistently. But after a few years, I slowly started noticing something uncomfortable. Even though I was saving regularly, my money didn’t feel like it was actually growing in a meaningful way.

Meanwhile- Rent kept increasing, Food prices became expensive, Travel costs went up and Everyday expenses slowly became heavier. That’s when I started understanding why many people eventually explore both fixed deposits and mutual funds instead of relying only on one option.

Not because one is “perfect.”

But because both solve different financial problems.

For more similar posts : –CLICK HERE

Why Fixed Deposits Feel Safe and Comfortable

There’s a reason millions of Indians still prefer fixed deposits. An FD gives emotional peace. You deposit money into the bank, and from day one, you already know- The interest rate, Maturity amount and Investment duration. There are no sudden market crashes. No daily price fluctuations. No panic.

For many people, especially first-generation earners, that stability matters a lot. Fixed deposits usually work well for people who-Need money within a short period, cannot tolerate financial stress, are building emergency savings, are retired or close to retirement and want predictable returns

For them, protecting money matters more than chasing higher returns and that is completely valid. One day, I decided to calculate something properly for the first time.I looked a FD returns, inflation,taxes and actual purchasing power.That’s when I realized something surprising. Even though my money was technically growing, the real growth after inflation and tax was much smaller than I expected.

For example:

If an FD gives around 6–7% returns, but inflation itself is increasing by 5–6%, the actual difference becomes very limited over time. Your money may stay safe — but its purchasing power may not increase significantly.

That realization changed how I looked at long-term investing.

I remember my first FD clearly. I put ₹1 lakh in IDFC First Bank for 2 years. At the time it felt like a smart, responsible decision. When it matured, I saw the number had grown and genuinely felt good about it. But then I just casually checked what a flexi cap mutual fund had done in those same 2 years — and that’s when the uncomfortable feeling started. My money had grown. But it had grown quietly, slowly, just enough to feel safe. Not enough to actually change anything.

What Mutual Funds Actually Are

When many beginners hear the term “mutual funds,” they immediately think :-

- “Stock market”

- “Too risky”

- “I might lose money”

I used to think the same way. But mutual funds are simply investment vehicles where money from many investors gets pooled together and managed by professional fund managers. Depending on the type of fund, the money may be invested into-

- stocks

- bonds

- government securities or a combination of different assets

Fixed Deposits offer Fixed income, unlike them mutual funds do not guarantee any returns. Some years can deliver strong growth. Some years can be disappointing. That uncertainty is what scares many first-time investors.

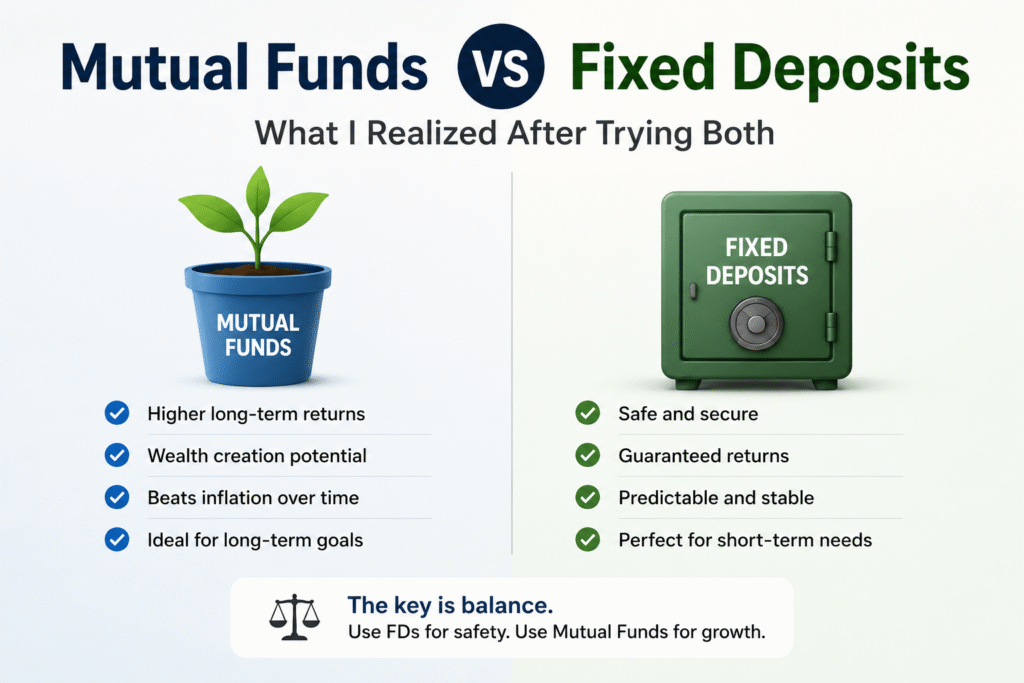

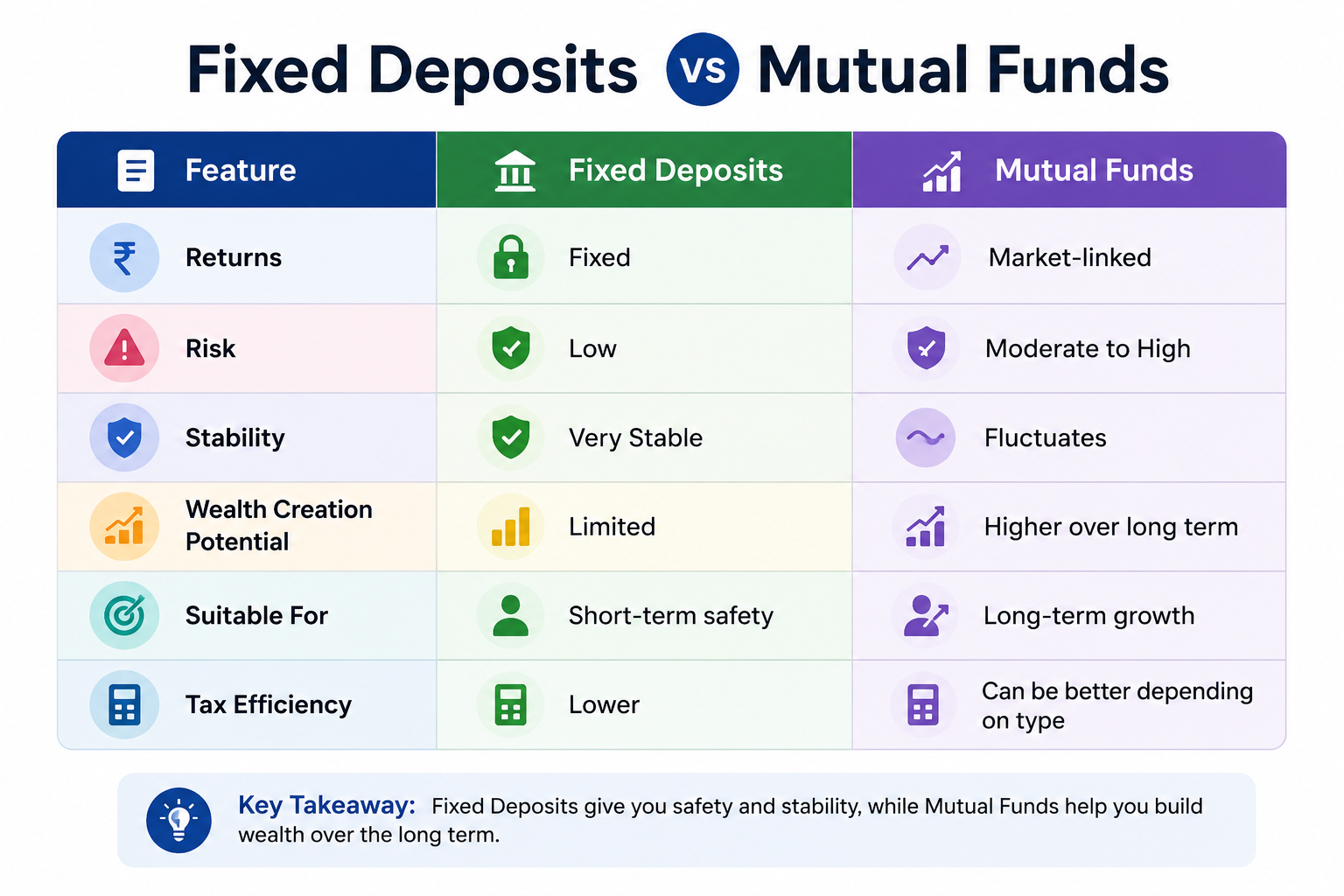

FD vs Mutual Funds: The Basic Difference

Fixed deposit is for fixed returns whereas mutual fund is market linked return.

The above image shows the exact difference between fixed deposit & Mutual funds. This is why comparing them directly can sometimes be misleading. They are built for different goals.

The Biggest Mistake Beginners Make

After spending time reading finance content online, I noticed one dangerous pattern. Social media has made investing look unrealistically easy. You constantly see- “This mutual fund gave 25% returns”, “My SIP doubled” and “Invest ₹5,000 and become rich”

But very few people talk about – market corrections, patience, emotional discipline and long-term consistency Many beginners invest during excitement and then panic when markets fall. That usually creates disappointment. The problem is not always mutual funds. Sometimes the problem is unrealistic expectations.

Why Fixed Deposits Still Matter

One thing I understood over time is that financial decisions are not only about numbers. Peace of mind matters too. Some people simply cannot handle seeing investments fluctuate every month. Even if long-term returns are better elsewhere, they may still prefer stability. Personal finance is personal. If someone sleeps peacefully knowing their money is safe in an FD, that itself has value.

Why Many Younger Investors Prefer Mutual Funds for Long-Term Goals

At the same time, avoiding growth completely can create future problems too. Long-term goals are becoming more expensive every year. Things like- buying a house, retirement planning, children’s education and financial independence

usually require stronger long-term growth than traditional savings alone can provide. Historically, equity mutual funds have delivered better long-term returns compared to traditional fixed deposits, although they also come with higher risk and volatility. That’s why many younger investors now combine:

safe savings with growth-oriented investments instead of depending only on one option.

What I Personally Noticed About Successful Investors

The most real example I have is my father. He’s not someone who checks his investments every week or talks about market trends at the dinner table. He just quietly kept putting money aside — some in FDs, some in LIC, consistently, for years. No panic during market crashes. No excitement during bull runs. Just the same habit, month after month. And today he’s more financially secure than most people I know who were chasing returns. That taught me something — it’s not always about where you invest. It’s about whether you actually stay with it.

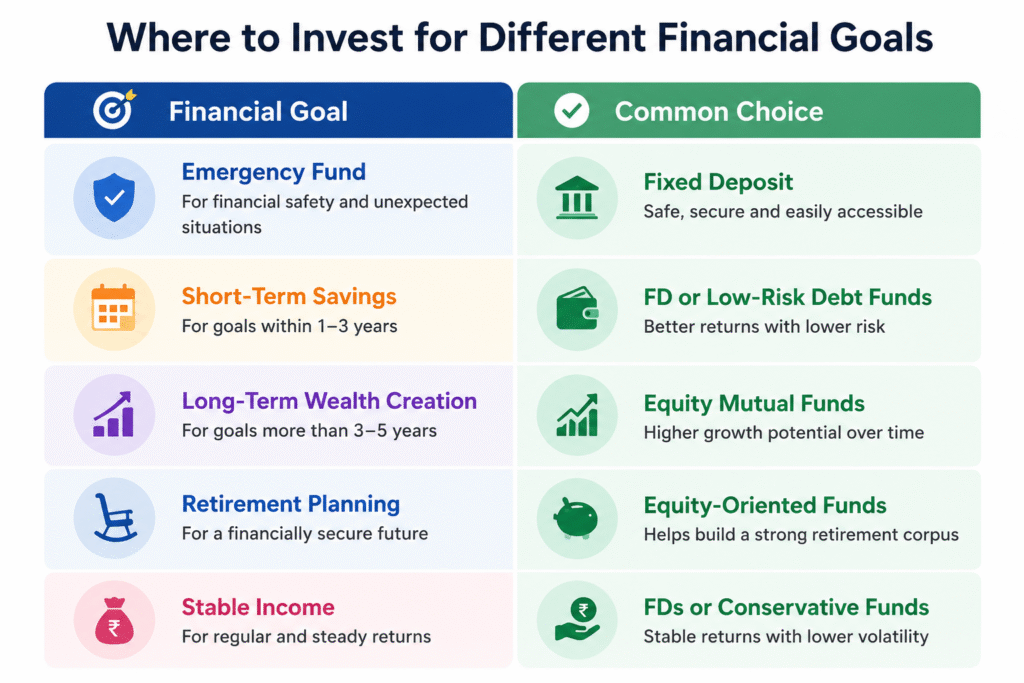

Earlier, I thought investing meant choosing one side. Either mutual fund or Fixed deposit, but some investors invest in both.

But real financial planning rarely works like that. Most people eventually divide money based on purpose.

So Which One Is Better?

Honestly, that is probably the wrong question. A better question is:

“What does this money need to do for me?” – If the money is needed soon, safety may matter more. If the goal is far away, growth may matter more. That is the real difference between fixed deposits and mutual funds.

Final Thoughts

For years, I believed fixed deposits were the smartest solution for every financial goal. Now I see things differently. Fixed deposits are excellent for stability and safety. Mutual funds are useful for long-term wealth creation. Neither option is perfect for every situation. And most people probably don’t need to blindly choose only one.

The important thing is understanding- why you are investing, what your financial goal is and how much risk you can emotionally handle.

Because once those answers become clear, choosing where to put your money becomes much easier.

Disclaimer

This article is intended for educational purposes only and reflects personal experience. Kindly consider this as NOT Financial advice.

About the Author

I am Livin Rangasamy, NISM-certified professional and mutual fund distributor, focused on simplifying personal finance for beginners.

For Similar posts : –CLICK HERE

")

")